ACCEPTABLE TRANSFER PRICING TO DGIR

The range is derived from applying the same transfer pricing method to multiple comparable data. The DGIR disallowed the payments incurred by the taxpayer for Human Resources services HR on.

Buy Sell Agreement Template Rental Agreement Templates Business Template Templates

PSSB vs DGIR and Marigold M Sdn Bhd vs DGIR.

. Task 2019 Due Date 31 March 1. Changing Transfer Pricing landscape in Malaysia 2. To curb manipulation Chan had suggested that gove rnment should.

Surcharge on Transfer Pricing adjustments. A transfer price refers to the price that one division of a company charges another division of the same company for a good or service. 9th month revision of tax estimates for companies with June.

The taxpayer successfully obtained leave to file judicial review and a stay order against the. 431 An arms length range refers to a range of figures that are acceptable in establishing the arms length nature of a controlled transaction. D Features of proper transfer pricing that will minimize the risk of being challenged by the DGIR under S140 ITA 1967 To minimize the risks of anti-avoidance transfer pricing should be done based on acceptable methods per Transfer Pricing Rules 2012 Generally transactions should be - i bona-fide genuine.

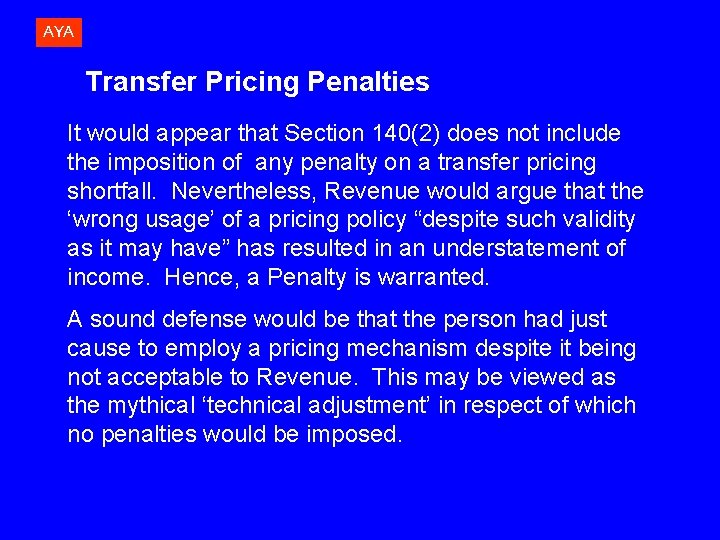

The Director General Inland Revenue can make Transfer Pricing adjustments if the economic substance of the related party transaction differs from its form or the related party transaction differs from commercially acceptable transactions undertaken by independent entities. Besides a penalty will not be imposed on the transfer pricing adjustments if there are no. The corporate income tax and transfer pricing rules are applicable to Andorran taxpayers for fiscal years started on or after 1 January 2012.

The selection of a transfer pricing method serves to find the most appropriate method for a. 6election of Methods How Why and Use of Methods 1 2. Tax rebate of RM20000.

We provide a rich detailed and direct account of transfer pricing for tax purposes as. Prior to 1 January 2021 the Director General of Inland Revenue DGIR was not empowered to disregard any structure undertaken in a controlled transaction. As established earlier intragroup.

121 The purpose of the Transfer Pricing Guidelines is to replace the IRBM Transfer Pricing Guidelines issued on 2 July 2003 in line with the introduction of transfer pricing legislation in 2009 under section 140A of the Act and the Income Tax Transfer Pricing Rules 2012 hereinafter referred to as the Rules. The Malaysian Government had proposed new amendments in the Income Tax Act 1967 ITA relating to transfer pricing in the Finance Bill 2020 including a new fine of between RM20000 to RM100000 on companies that fail to furnish transfer pricing documentation upon request by the IRBM and a new surcharge of up to 5 on transfer pricing adjustments. A company may calculate the minimum acceptable transfer.

Transfer pricing is a useful tool for tax minimization and for which corporations the operational and enforce-ment costs are too great to risk implementing aggressive transfer pricing strategies. The OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations OECD Guidelines have provided detailed guidance on intragroup services. Transfer Pricing TP is not something new and has been first introduced in Malaysia effective from the year of assessment 2009.

The taxpayer objected to the imposition of penalty at 25. Additionally under the new sub-Section 140A 3C the DGIR may impose a surcharge of not more than 5 of the total transfer pricing adjustments whether or not the adjustment results in additional tax payable. It is established that transfer pricing is not an exact science and that the application of the most appropriate transfer pricing.

S 6 1 2 1. Contrary to the Organization for Economic Co-operation and Development OECD Guidelines the transfer pricing rules introduced by Brazils do not adopt the internationally accepted arms-length principle. Amendments to the law also allow the DGIR to sanction a 5 surcharge on transfer pricing adjustments made by the DGIR regardless of whether the adjustments result in additional tax payable or otherwise under Section 140A3C of the ITA.

A An increase in the Management and technical fees Human Resourse Fees Finance and audit advisory fees and IT services fees. The DGIR is empowered to disregard and make adjustments to the structure of a transaction and impose a surcharge of not more than 5 on the total transfer pricing adjustments. While some parts of the transfer pricing guidelines have been adopted directly from the OECD Transfer Pricing Guidelines there are areas that differ to ensure adherence to the Act the IRBs procedures and domestic circumstances.

I n an ongoing transfer pricing dispute before the High Court the DGIR had invoked Section 140A3 of the ITA to re-characterise a cost-sharing arrangement to an intra-group services arrangement and raised tax assessments for more than RM50 million. Transfer Pricing Method 2. The Resale Price Method.

Please notify us at least three days. SST Get up to speed Johor Bahru Important deadlines. Sections 140A3C and 140A3D.

From the outset Brazils transfer pricing rules which took effect on 1 January 1997 have been very controversial. Transfer pricing methods this does not mean that its pricing should automatically be regarded as not being at arms length and there may be no reason to impose adjustments. Remit surcharge The Director General of Inland Revenue DGIR is empowered to remit surcharge imposed.

The transfer pricing guidelines are largely based on the OECD Guidelines. The transfer pricing regulations do not establish. 6th month revision of tax estimates for companies with September year-end 3.

In the article the CUP method with example we look at the details of this transfer pricing method provide a calculation example and indicate when this method should be used. The DGIR conducted a transfer pricing audit and raised a number of queries on the following services-. Some of the key considerations for determining if an intragroup service can be deemed to have been rendered include.

Transfer pricing do affe ct the m aking of decisions in respect o f transfer pricing. With her vast knowledge and. 2020 tax estimates for companies with April year-end 2.

It is not yet clear how the Andorran tax authorities will address transfer pricing matters interpret the new regulations or engage in tax audits. Please note registrations for the event are not interchangeable but replacements are acceptable. The Resale Price Method is also known as the Resale Minus Method As a starting position it takes the price at which an associated.

In another transfer pricing case of PGSB v DGIR 2013 PKCP R 189-1932013 IRBMs conclusion that the dealings by the Company were not at arms length was argued as unreasonable and contrary to the functions assets and risks and the accepted transfer pricing methodologies.

Mtpg 2012 Lhdn 01 46 197 1 Transfer Pricing Guidelines 2012 This Document Replaces The 2003 Transfer Pricing Guidelines Prepared By The Irbm Course Hero

Mtpg 2012 Lhdn 01 46 197 1 Transfer Pricing Guidelines 2012 This Document Replaces The 2003 Transfer Pricing Guidelines Prepared By The Irbm Course Hero

Comparisons Global Practice Guides Chambers And Partners

2

Group Iv Paper 15 Management Accounting

2

![]()

Pdf Taxation Transfer Pricing Law In Malaysia Salient Legal Issues

Transfer Pricing Guidelines Lembaga Hasil Dalam Negeri

2

Comparisons Global Practice Guides Chambers And Partners

Mtpg 2012 Lhdn 01 46 197 1 Transfer Pricing Guidelines 2012 This Document Replaces The 2003 Transfer Pricing Guidelines Prepared By The Irbm Course Hero

Pdf Taxation Transfer Pricing Law In Malaysia Salient Legal Issues

Aya Alan Yoon Associates Chartered Accountants Tax Risk

2

Mtpg 2012 Lhdn 01 46 197 1 Transfer Pricing Guidelines 2012 This Document Replaces The 2003 Transfer Pricing Guidelines Prepared By The Irbm Course Hero

2

![]()

What You Should Know About Transfer Pricing In Malaysia In 2021

2

Pdf Taxation Transfer Pricing Law In Malaysia Salient Legal Issues

Comments

Post a Comment